AI is already transforming the way we work, boosting productivity and efficiency. Just as we moved from horses to motorcars or jobs done by hand to computers, AI represents the next generational shift in productivity. During my recent meetings in California with the senior management of over a dozen companies, one term consistently emerged: “AI Agents.”

While being a great buzzword for the next generation of AI productivity and support, it is important to understand what an AI Agent really is and who the winners and losers will be. A good starting point is to de-bunk some of the misconceptions between Co-Pilots and AI Agents.

Co-Pilot versus AI Agents: What is What!

With the convergence of large language models (LLMs) and chat interfaces, the creation of Co-Pilots – AI assistants designed to aid productivity and creativity – have seen a rapid rise in usage. Co-Pilots leverage Natural Language Processing to understand and generate text. This process involves breaking down input text into tokens, known as tokenisation, which models then process to generate responses.

Initially, Co-Pilots operated through text, but have since evolved to support multimodal inputs and outputs such as images and videos. Although still in its infancy, scepticism persists due to the currently limited real-world applications for Co-Pilots in an enterprise setting. One notable limitation has been the tendency for Co-Pilots to produce erroneous facts or famously fabricate cases in legal research which have been submitted to court. Grounding is now an option for supported models to reduce model hallucinations and to anchor model responses to verifiable sources of information. Models can be grounded to publicly available data or tethered to specific private datasets, significantly improving accuracy and reliability.

Technically speaking, a Co-Pilot is a type of agent. However, the distinction between Co-Pilots and AI Agents lies in their interaction and autonomy. While Co-Pilots work alongside users, requiring input and interaction, AI Agents can operate autonomously, adapting and learning independently. This autonomy is what makes AI Agents so exciting.

As AI Agents operate totally independently, they are capable of managing complex tasks without continuous human intervention. For example, an AI Agent might manage your calendar, scheduling meetings but also being able to adjust them based on the availability of participants and other priorities, all the time without needing any input except of course where it has learned that you would like to be consulted! It is this adaptability that sets AI Agents aside, and they are designed to learn and adapt. They improve and evolve their behaviour with every interaction, providing better outcomes and dynamically changing with the environment. They will make informed choices by utilising vast amounts of data, streamlining workflows and ensuring the best possible outcomes.

There are limited applications of AI Agents in action today. Intuit, however, the online accounting software provider, has showcased Agent AI-powered workflows to assist in automating cash flow management, such as managing business postings and using specialised AI Agents to orchestrate invoice processing or bill creation. While ServiceNow, the market leading cloud-based software company that manages and optimizes enterprise workflows, envisions agent-to-agent collaboration that could address multi-departmental issues across workflows without the need for human intervention.

We are some way from multifarious use cases. The focus is currently on customer relationship management, think better and more autonomous chatbots for resolving customer interactions. There is also increasing use within various B2B applications where the agents operate in a more walled garden environment that is easier to manage.

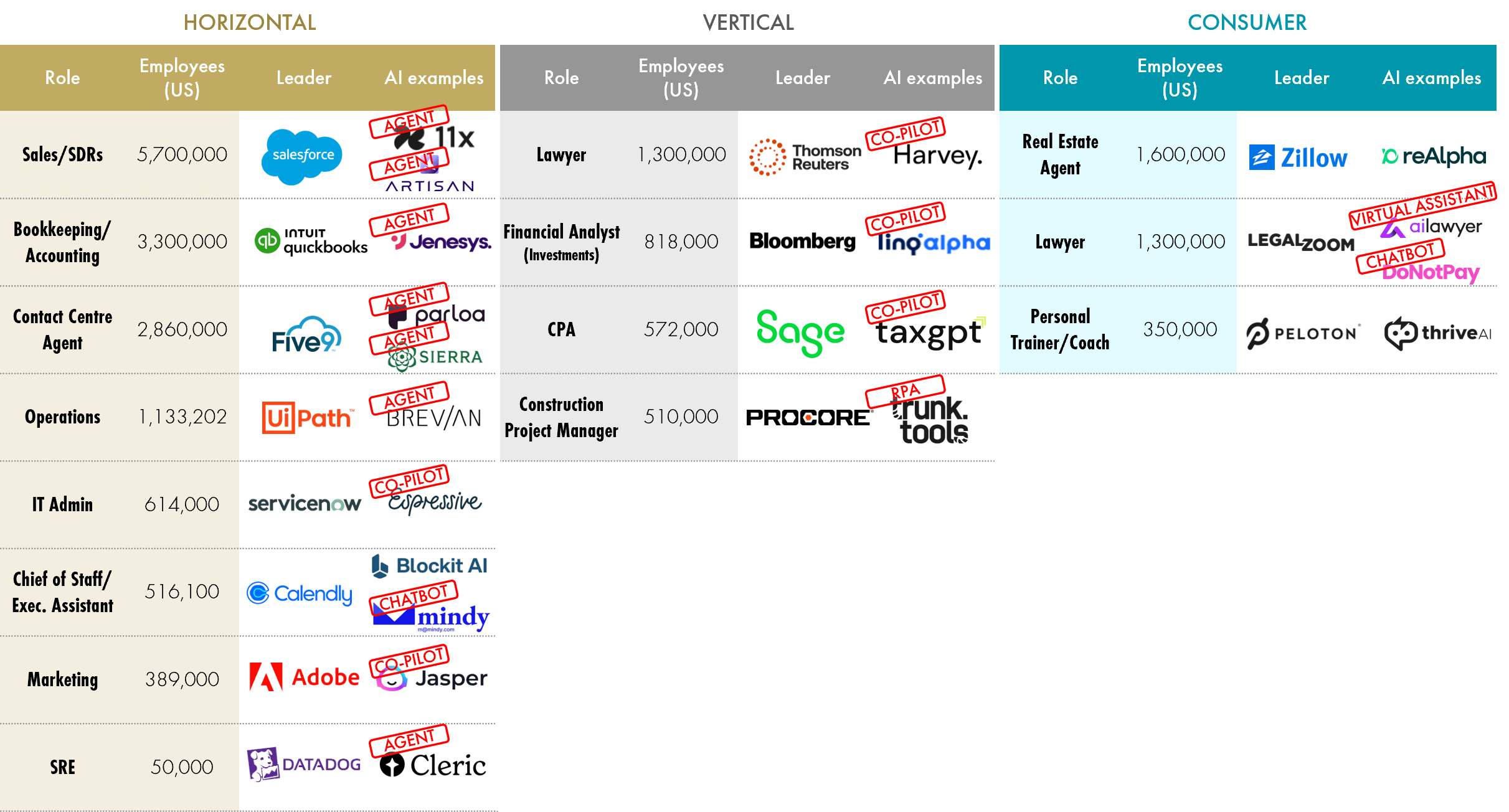

Confusion remains around where Co-Pilots end and AI Agents begin, most notably in some industry verticals or consumer facing applications. The table below is an extract from a larger data set published under the heading “The Agent Economy” (Felicis). We highlight in the final column our view on the true classification of these disrupters.

Source: www.felicis.com/insight/the-agent-economy and Liontrust, October 2024. RPA = Robotic Process Automation. All use of company logos, images or trademarks in this document are for reference purposes only.

While some of the new companies in the right hand column are Agent AIs, especially in the horizontal provider category, those in industry verticals and consumer are largely Co-Pilots or RPA companies (Robotic Process Automation). Some even overclaim their ability! Recently, DoNotPay ageed to a $193,000 settlement with the Federal Trade Commission (FTC), after initially claiming to “generate perfectly valid legal documents in no time.” DoNotPay stated they would “replace the $200-billion-dollar legal industry with artificial intelligence,” however they did not conduct any testing to compare outputs to a human lawyer and did not have any attorneys. The company is now prohibited from making claims about its ability to substitute professional services without any evidence to back it up.

The confusion is such that, for example, reAlpha, an agent in the property investment field, came to the stock exchange in late 2023 (six months after the Nvidia Eureka moment) with disastrous consequences. Hailed as an AI agent with great potential, it conducted a direct listing at $8 per share as the reference price. It opened at $23 and rallied on day one to close at $407!! This left the founder, CEO Giri Devanur, with a paper fortune of $11.2 billion. Days later, the shares had crashed and today the shares trade at $1 and with a market value of just $54 million. This should act as a stark reminder of hype versus reality. We don’t doubt the potential but as with all new technologies, care is needed.

RPA is also often confused with Agent AI. This industry sub-sector came to prominence in 2012, and the first high-profile company was Blue Prism listed on the UK Stock Exchange. US companies followed, with the most high profile of these being UI Path that listed in 2022 at a price of $56. It quickly rose to $90 on AI hype but has since fallen back to $12.5, a fall of 86% from the peak. RPA has gone from AI boom to little more than a rules-based assistant.

It is estimated that over time, AI Agent’s will resolve 80% of inquiries autonomously, allowing human employees to focus on more complex projects1, while Gartner predicts that, by 2028, one third of interactions with GenAI services will invoke action models and autonomous agents for task completion.

1. Zendesk: www.zendesk.co.uk/blog/ai-agents/#georedirect

Will AI Agents drive a change in pricing strategies?

With AI’s growing impact, the question arises of how AI Agents can monetise the value they create. In the early days of software, perpetual licenses with optional maintenance and support fees were common. However, this model has largely been phased out in favour of a seat-based or consumption-based model or a blend of these two. Seat based offers lower initial costs and greater flexibility for users, whereas usage-based models allow customers to pay based on their actual usage and throughput. With AI Agents, given the cost of compute, a number of companies are experimenting with work-based pricing models. ServiceNow is considering the use of tokens for additional compute resources on top of their existing model. Salesforce recently announced a charge of $2 per conversation handled by its AI agents – helping to mitigate the possible impact of AI agents cannibalising their current model with labour efficiency.

When transformative technologies emerge, they typically attract vast amounts of capital and intense competition. However, caution is necessary. Marc Benioff, CEO and Co-Founder of Salesforce, recently criticised the hype as selling science projects to companies and comparing Microsoft Co-Pilot to the infamous Microsoft Clippy. The opportunity is clear but the speed of adoption is not.

Company valuations can often stray from fundamentals, with an overestimation of return on invested capital by the first movers. As data quality improves and models gain access to private company data, the integration of AI agents into existing workflows will significantly increase productivity and efficiency. This opportunity excites us; we are early in the innings for AI and the real enterprise use cases are just starting to emerge.

KEY RISKS

Past performance is not a guide to future performance. The value of an investment and the income generated from it can fall as well as rise and is not guaranteed. You may get back less than you originally invested.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

The Funds managed by the Global Equities team:

May hold overseas investments that may carry a higher currency risk. They are valued by reference to their local currency which may move up or down when compared to the currency of a Fund. May encounter liquidity constraints from time to time. The spread between the price you buy and sell shares will reflect the less liquid nature of the underlying holdings. May have a concentrated portfolio, i.e. hold a limited number of investments or have significant sector or factor exposures. If one of these investments or sectors / factors fall in value this can have a greater impact on the Fund's value than if it held a larger number of investments across a more diversified portfolio. May invest in smaller companies and may invest a small proportion (less than 10%) of the Fund in unlisted securities. There may be liquidity constraints in these securities from time to time, i.e. in certain circumstances, the fund may not be able to sell a position for full value or at all in the short term. This may affect performance and could cause the fund to defer or suspend redemptions of its shares. May invest in emerging markets which carries a higher risk than investment in more developed countries. This may result in higher volatility and larger drops in the value of a fund over the short term. Certain countries have a higher risk of the imposition of financial and economic sanctions on them which may have a significant economic impact on any company operating, or based, in these countries and their ability to trade as normal. Any such sanctions may cause the value of the investments in the fund to fall significantly and may result in liquidity issues which could prevent the fund from meeting redemptions. May hold Bonds. Bonds are affected by changes in interest rates and their value and the income they generate can rise or fall as a result; The creditworthiness of a bond issuer may also affect that bond's value. Bonds that produce a higher level of income usually also carry greater risk as such bond issuers may have difficulty in paying their debts. The value of a bond would be significantly affected if the issuer either refused to pay or was unable to pay. Outside of normal conditions, may hold higher levels of cash which may be deposited with several credit counterparties (e.g. international banks). A credit risk arises should one or more of these counterparties be unable to return the deposited cash. May be exposed to Counterparty Risk: any derivative contract, including FX hedging, may be at risk if the counterparty fails. Do not guarantee a level of income. May, under certain circumstances, invest in derivatives, but it is not intended that their use will materially affect volatility. Derivatives are used to protect against currencies, credit and interest rate moves or for investment purposes. There is a risk that losses could be made on derivative positions or that the counterparties could fail to complete on transactions. The use of derivatives may create leverage or gearing resulting in potentially greater volatility or fluctuations in the net asset value of the Fund. A relatively small movement in the value of a derivative's underlying investment may have a larger impact, positive or negative, on the value of a fund than if the underlying investment was held instead. The use of derivative contracts may help us to control Fund volatility in both up and down markets by hedging against the general market. The use of derivative instruments that may result in higher cash levels. Cash may be deposited with several credit counterparties (e.g. international banks) or in short-dated bonds. A credit risk arises should one or more of these counterparties be unable to return the deposited cash.

The risks detailed above are reflective of the full range of Funds managed by the Global Equities team and not all of the risks listed are applicable to each individual Fund. For the risks associated with an individual Fund, please refer to its Key Investor Information Document (KIID)/PRIIP KID.

DISCLAIMER

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID), which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.co.uk or direct from Liontrust. Always research your own investments. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.

This should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, forwarded, reproduced, divulged or otherwise distributed in any form whether by way of fax, email, oral or otherwise, in whole or in part without the express and prior written consent of Liontrust.