A group of barren, uninhabited volcanic islands near Antarctica – the Heard and McDonald Islands – both covered in glaciers and home only to penguins, had a 10% tariff on goods imposed on them yesterday by Trump’s executive order. This, despite no human visitors in nearly 10 years…so goes the US’s new tariff agenda.

The “reciprocal” tariff policy announced was unprecedented in recent history and imposes a weighted average tariff rate of 18.3%, raising the effective tariff rate to levels not seen since the pre-war period when the Smoot-Hawley Tariff Act was introduced. A reminder that Smoot-Hawley is often cited as a major trigger for the ensuing Great Depression (see chart below), which was only relieved by the onset of the Second World War.

Source: Bloomberg, April 2025

Given that only roughly one-third of total imports would be exempt, this reduces the tariff impact to a 12.6 percentage point increase in the effective tariff rate. While negotiations with trading partners could well lead to somewhat lower “reciprocal” rates than announced today, the prospect for escalation following retaliatory tariffs and a high probability of further sectoral tariffs suggests a risk that the US effective tariff rate rises further.

Source: Goldman Sachs, 2025

Our View

These tariffs have gone well beyond what was priced in for most regions (ex-India). There are still a few days before they come into effect, so some are questioning whether this provides a (short) window for negotiation. But at this point, that may be more hope than reality from groups that believed Trump would never go this far. More likely, we are entering a tit-for-tat escalation.

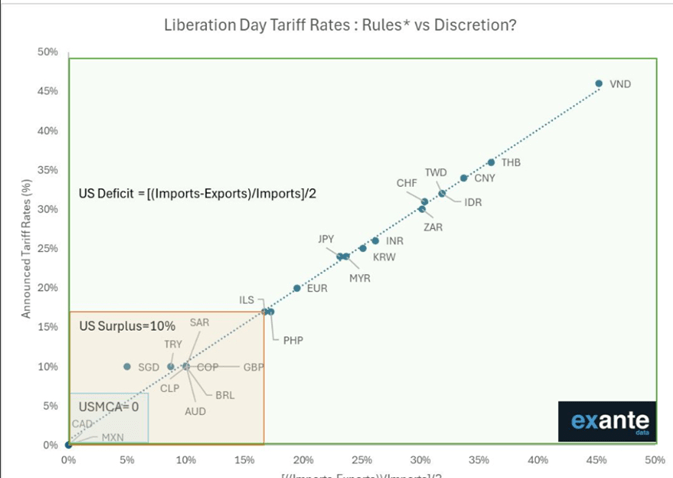

It is also interesting to note that the tariff rates set yesterday appear to be perfectly correlated with US bilateral trade deficits (chart below). This implies that the goal is simply to reduce such deficits – an election promise made by Trump. If so, it lessens the likelihood that any negotiations will be forthcoming.

Source: Exante Data

What does this mean for global markets?

Japan

Often seen as a geared play on global growth and has thus been hit quite hard as recession risks rise. Banks are particularly weak, as weaker economic conditions challenge the Bank of Japan’s (BoJ) ability to raise rates.

India

India appears to have come out “well” from yesterday’s developments, confirming the assumption that it is a safe port in a tariff storm. That has worked against it somewhat, as tariff fears have receded year-to-date, but could now act as support. No incremental adverse impact on export sectors (IT services, pharma, autos). Reciprocal tariffs at 27% are unhelpful, but India is a relative winner within Asia. The market was only off -0.3%. However, there were big internal moves – IT services (a proxy on US corporate spend) down significantly, pharma up sharply. There had been major concerns on both, but the negative US outlook is overwhelming any relief rally for IT & pharma.

Interestingly, after a period of relative weakness, the Indian market is trading well and has begun to show signs of relative strength versus China and Japan.

Latin America

Latin America is relatively insulated and sits at the low end of the tariff spectrum – all countries are at the base 10% rate, with Mexico (and Canada) continuing to benefit from USMCA exemptions. While a global recession would clearly not be helpful, the region has been supported by a weaker US Dollar, which is helping to lower domestic inflation expectations and could allow for additional rate cuts, or earlier cuts in Brazil’s case. The Mexican Peso (MXN) is up 2%, and stimulus is expected to follow once tariffs are in place, which may partly explain the region’s resilience.

Overall, Latin America should fare well on a relative basis given its greater exposure to China than to the US. If China responds with more stimulus, it could offset some of the negative tariff impact. For Mexico, attention is focused on the renegotiation of the USMCA, which is likely to begin ahead of schedule (previously set for next year). While Trump has repeatedly criticised NAFTA, he has not addressed its replacement, USMCA, which he signed during his first term. MSCI Mexico is up 2% pre-market, largely driven by peso strength, and Mexico's competitive position versus Asian exporters has improved further.

China/Asia

The 34% tariff is higher than expected, up from the 20% announced in February and March. It also includes imports from Hong Kong and Macau. Exporters are being hit as expected, but domestic names in China are largely flat today – encouraging, with the presumption being that the next leg of consumption stimulus will follow after the tariffs are in place, contributing to the resilience.

Most of the US’s Asian trading partners are facing higher-than-expected tariffs, including Vietnam (46%), Taiwan (36%), Thailand (36%), and Indonesia (32%). Sports apparel brands that manufacture in Vietnam, such as Lululemon (-10%) and Nike (-6%), are being heavily impacted.

Gold

Gold benefits from safe-haven demand and acts as a hedge against inflation. The tariffs add friction to global trade flows and will increase inflationary pressure. The weaker US Dollar also helps stimulate gold demand. Gold remains on a strong upward trajectory, and we see no reason for this to change following these announcements.

KEY RISKS

Past performance is not a guide to future performance. The value of an investment and the income generated from it can fall as well as rise and is not guaranteed. You may get back less than you originally invested.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

The Funds managed by the Global Equities team:

May hold overseas investments that may carry a higher currency risk. They are valued by reference to their local currency which may move up or down when compared to the currency of a Fund. May encounter liquidity constraints from time to time. The spread between the price you buy and sell shares will reflect the less liquid nature of the underlying holdings. May have a concentrated portfolio, i.e. hold a limited number of investments or have significant sector or factor exposures. If one of these investments or sectors / factors fall in value this can have a greater impact on the Fund's value than if it held a larger number of investments across a more diversified portfolio. May invest in smaller companies and may invest a small proportion (less than 10%) of the Fund in unlisted securities. There may be liquidity constraints in these securities from time to time, i.e. in certain circumstances, the fund may not be able to sell a position for full value or at all in the short term. This may affect performance and could cause the fund to defer or suspend redemptions of its shares. May invest in emerging markets which carries a higher risk than investment in more developed countries. This may result in higher volatility and larger drops in the value of a fund over the short term. Certain countries have a higher risk of the imposition of financial and economic sanctions on them which may have a significant economic impact on any company operating, or based, in these countries and their ability to trade as normal. Any such sanctions may cause the value of the investments in the fund to fall significantly and may result in liquidity issues which could prevent the fund from meeting redemptions. May hold Bonds. Bonds are affected by changes in interest rates and their value and the income they generate can rise or fall as a result; The creditworthiness of a bond issuer may also affect that bond's value. Bonds that produce a higher level of income usually also carry greater risk as such bond issuers may have difficulty in paying their debts. The value of a bond would be significantly affected if the issuer either refused to pay or was unable to pay. Outside of normal conditions, may hold higher levels of cash which may be deposited with several credit counterparties (e.g. international banks). A credit risk arises should one or more of these counterparties be unable to return the deposited cash. May be exposed to Counterparty Risk: any derivative contract, including FX hedging, may be at risk if the counterparty fails. Do not guarantee a level of income. May, under certain circumstances, invest in derivatives, but it is not intended that their use will materially affect volatility. Derivatives are used to protect against currencies, credit and interest rate moves or for investment purposes. There is a risk that losses could be made on derivative positions or that the counterparties could fail to complete on transactions. The use of derivatives may create leverage or gearing resulting in potentially greater volatility or fluctuations in the net asset value of the Fund. A relatively small movement in the value of a derivative's underlying investment may have a larger impact, positive or negative, on the value of a fund than if the underlying investment was held instead. The use of derivative contracts may help us to control Fund volatility in both up and down markets by hedging against the general market. The use of derivative instruments that may result in higher cash levels. Cash may be deposited with several credit counterparties (e.g. international banks) or in short-dated bonds. A credit risk arises should one or more of these counterparties be unable to return the deposited cash.

DISCLAIMER

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID), which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.co.uk or direct from Liontrust. Always research your own investments. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.

This should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, forwarded, reproduced, divulged or otherwise distributed in any form whether by way of fax, email, oral or otherwise, in whole or in part without the express and prior written consent of Liontrust.