We are always trying to find new ways of illustrating the resilient, income-generating nature of high yield bonds, and this table – a format we’ve adapted from some equity research we saw recently – does exactly that.

Source: Liontrust, Bloomberg, ICE BofA Global High Yield Index. As at 31.08.24. US dollars.

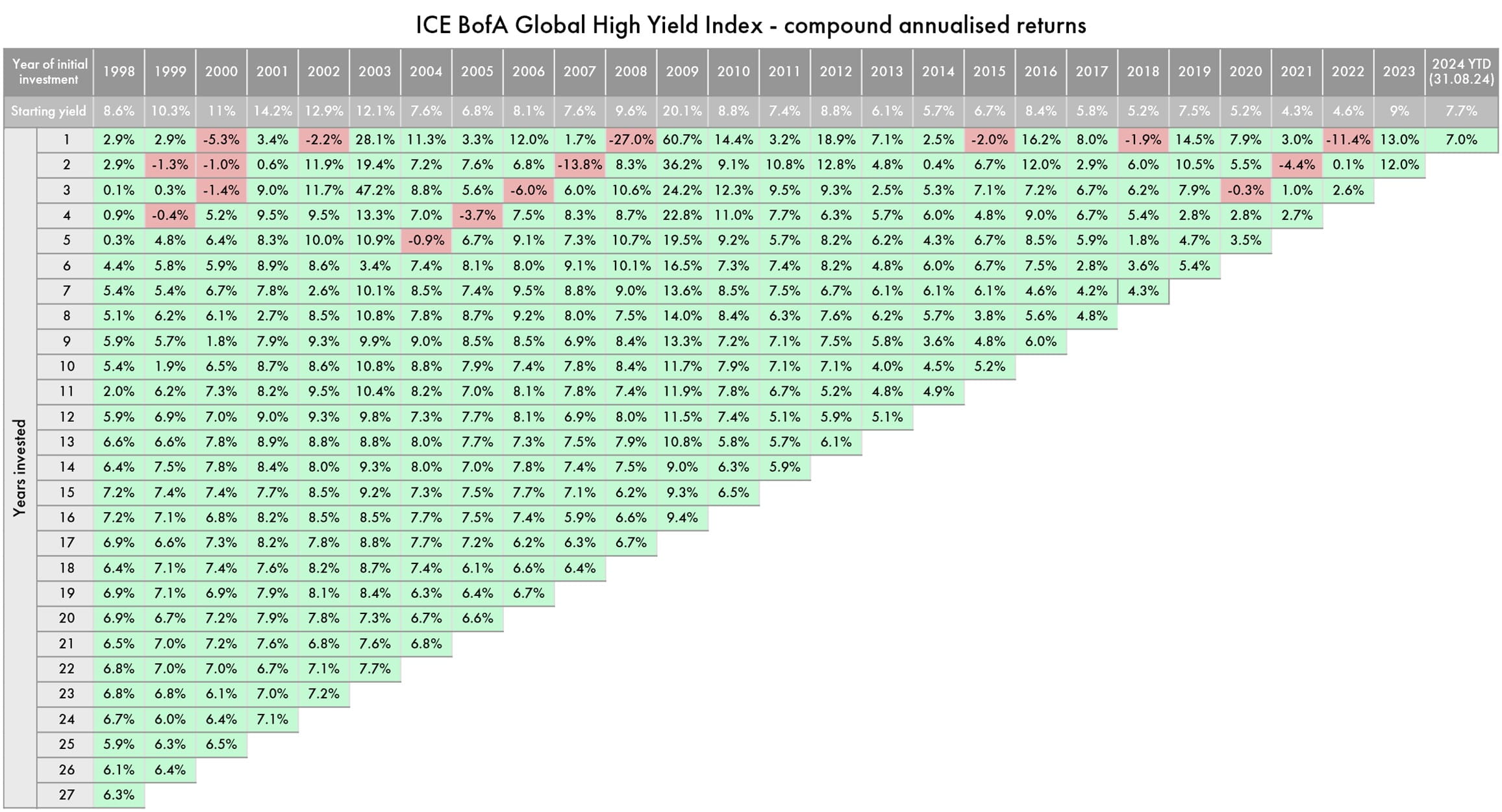

The table shows the calendar year of initial investment across the top, with the subsequent annualised compound returns dropping down vertically beneath it, with a maximum investment period of 27 years (including 2024 year-to-date) since 1998.

While there is a lot of data to assimilate here, which may be trickier on smaller screens, I think it is well worth the effort to zoom in as it does a really effective job of showing the characteristics of the asset class over an eventful period.

A few initial observations

- Over the full 27-year dataset, an investor buying into high yield bonds at the start of 1998 would have received a compound annual return of 6.3%, without their investment ever dipping into the red.

- Of the 27 calendar years, only six investment returns were negative: 2000, 2002, 2008, 2015, 2018 and 2022.

- On five of these occasions, the high yield market staged a bounce back strong enough that the loss was more than recouped the following year. For example, an investor buying at the start of 2008 would have suffered a 27% loss in their first year; but in 2009 the market rallied by 60.7%, taking the two-year return (for the 2008 investor) to 8.3%.

- It was only the 2000 calendar year loss that took more than a year to recover from. Investors had to wait four years before they returned to a 5.2% positive annualised return overall (boosted by the 28% rally in 2003).

- Out of the entire dataset, there was only one period longer than this in which investors had to endure negative overall returns: the five years from 2004 to 2008. Although modest positive returns were recorded from 2004 to 2007, this was wiped out by the -27% return as the global financial crisis hit in 2008, leaving five-year investors from 2004 with a -0.9% annualised return.

As already commented, the following year saw a bounce back which pushed six-year annualised returns immediately back up to 7.4%. - Even though this 2004 cohort would have endured a five-year period over which they had negative returns, their total return since this date has been uniformly positive and, by holding through to 2024, they would record a 6.8% average return (including the negative years).

- The 2005, 2006, and 2007 high yield investor cohorts were also affected by the large negative return in 2008 to the extent that total annualised returns briefly dipped into the red (for four-year, three-year and two-year periods respectively). But all bounced back the following year.

Considering these observations in a bit more detail, I think some key attractions of the high yield asset class clearly shine through in the data.

Short-dated nature of high yield restricts price falls

Firstly, one of the reasons there are so few red cells in the chart is that high yield is a naturally short-dated asset class. Because the average loan term is low, so too is duration – the level of bond price sensitivity to interest rate or credit spread changes.

While longer-duration government bonds might see a large price drop in order to reflect rising interest rate expectations, the impact of this discount rate change is smaller for short-duration bonds such as the typical high yield bond. In bond terminology, there is strong ‘pull to par’ within these short-dated bonds; while prices may dip below their par value, the short time to redemption at par will limit the extent of the deviation.

By definition, these high yield bonds also have a high annual income level for investors. This means that it takes quite a large bond price fall to outweigh the income in total return terms and – as we’ve established – these bond prices tend to fall less when interest rates rise.

The same is true of periods of widening credit spreads – the extra yield investors require for lending to higher risk companies rather than low-risk governments. If yields are rising due to wider credit spreads (as opposed to higher central bank rate expectations) the price reaction is still determined by duration (albeit it may be called ‘spread duration’), which – once again – is typically lower for high yield bonds than other bonds.

The best annual returns tend to be snap backs from poor years

It is also noticeable that some of the best annual returns came in immediate ‘snap backs’ after negative years, when prices were depressed and starting yields were commensurately higher. This suggests that starting yield is a good indicator of the level of value on offer in the market. Looking at 2024’s starting yield, we find a level of 7.7%, somewhere near the middle of the range of yields since 1998, supporting our view that the market is currently around fair value.

Defaults hit specific areas hard, but the impact is small across the asset class

What the chart doesn’t show in too much detail is the impact of defaults, when investors lose chunks of capital on companies unable to make interest and/or capital repayments. When averaged across the market, these defaults have a fairly small impact on annual total returns when compared with price fluctuations due to changes in interest rates and credit spreads.

For the areas they do affect, defaults clearly have a large negative impact on portfolio returns. When they happen, defaults are often concentrated in certain areas of the market. The turmoil at the beginning of the century, for example, had a problem child in the form of the telecoms sector whereas the 2015 selloff saw defaults focused on energy and commodities.

Minimise default risk by avoiding accumulations of thematic risk

While the market on the whole may look like it is offering decent value, we think it remains essential to avoid accumulations of thematic risk and default concentration that would pull you into the long tail of negative returns in the high yield market.

Due to the nature of value-weighted indices, the sectors and companies which borrow the most will account for larger proportions of high yield indices. By following index weightings, this can actually mean taking on more risk in the form of lending to heavily indebted areas.

We are instead seeking true diversification through idiosyncrasy, and we are happy to ignore what the index is telling us to own. The confidence we have in what we do own for our clients should allow us to manage what tend to be only short-lived periods of draw-down and volatility.

KEY RISKS

Past performance is not a guide to future performance. The value of an investment and the income generated from it can fall as well as rise and is not guaranteed. You may get back less than you originally invested.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

The Funds managed by the Global Fixed Income Team:

Consider environmental, social and governance (""ESG"") characteristics of issuers when selecting investments for the Funds. May hold overseas investments that may carry a higher currency risk. They are valued by reference to their local currency which may move up or down when compared to the currency of a Fund. Hold Bonds. Bonds are affected by changes in interest rates and their value and the income they generate can rise or fall as a result; The creditworthiness of a bond issuer may also affect that bond's value. Bonds that produce a higher level of income usually also carry greater risk as such bond issuers may have difficulty in paying their debts. The value of a bond would be significantly affected if the issuer either refused to pay or was unable to pay. May encounter liquidity constraints from time to time. The spread between the price you buy and sell shares will reflect the less liquid nature of the underlying holdings. May, under certain circumstances, invest in derivatives, but it is not intended that their use will materially affect volatility. Derivatives are used to protect against currencies, credit and interest rate moves or for investment purposes. There is a risk that losses could be made on derivative positions or that the counterparties could fail to complete on transactions. The use of derivatives may create leverage or gearing resulting in potentially greater volatility or fluctuations in the net asset value of the Fund. A relatively small movement in the value of a derivative's underlying investment may have a larger impact, positive or negative, on the value of a fund than if the underlying investment was held instead. The use of derivative contracts may help us to control Fund volatility in both up and down markets by hedging against the general market. The use of derivative instruments that may result in higher cash levels. Cash may be deposited with several credit counterparties (e.g. international banks) or in short-dated bonds. A credit risk arises should one or more of these counterparties be unable to return the deposited cash. May invest in emerging markets which carries a higher risk than investment in more developed countries. This may result in higher volatility and larger drops in the value of the funds over the short term. May be exposed to Counterparty Risk: any derivative contract, including FX hedging, may be at risk if the counterparty fails. May target an absolute return. There is no guarantee that an absolute return will be generated over the time period stated in the fund objective or any other time period.

The risks detailed above are reflective of the full range of Funds managed by the Global Fixed Income Team and not all of the risks listed are applicable to each individual Fund. For the risks associated with an individual Fund, please refer to its Key Investor Information Document (KIID)/PRIIP KID.

DISCLAIMER

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID), which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.co.uk or direct from Liontrust. Always research your own investments. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.

This should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, forwarded, reproduced, divulged or otherwise distributed in any form whether by way of fax, email, oral or otherwise, in whole or in part without the express and prior written consent of Liontrust.