- The second half of 2024 was challenging for the Fund due the headwind from a low large-cap value exposure as well as some stock-specific setbacks.

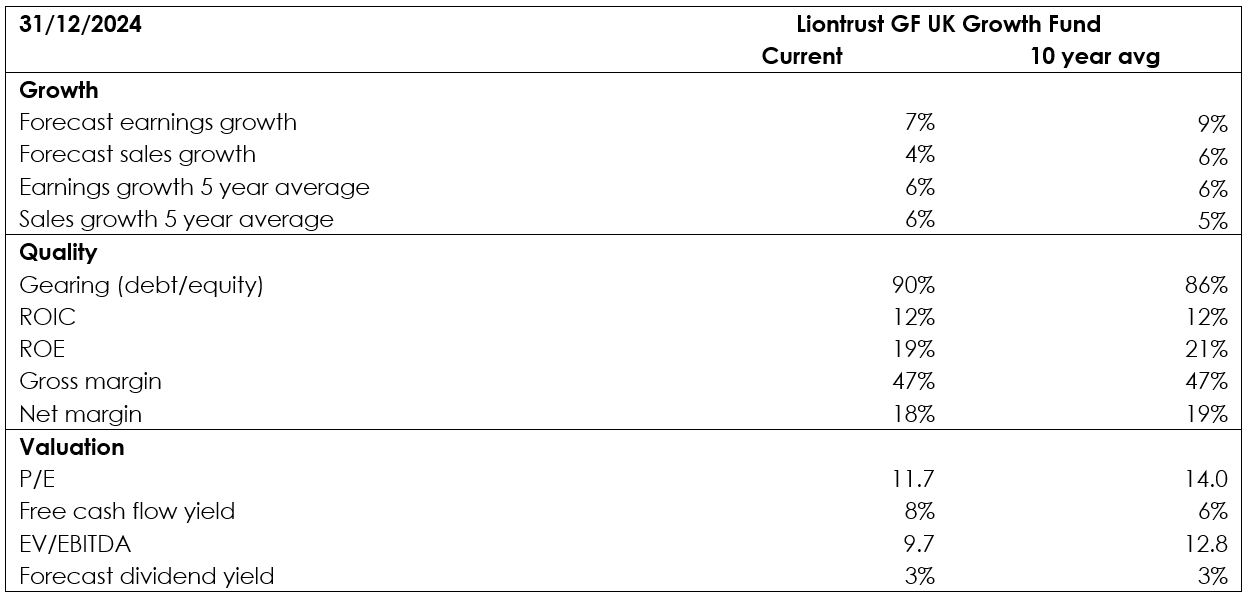

- The outlook is positive, with the Fund’s quality metrics at normal levels but valuations at a discount of around 14% to their long-term average.

- The portfolio is expected to deliver around 7% earnings growth next year, with a healthy dividend yield of 3%.

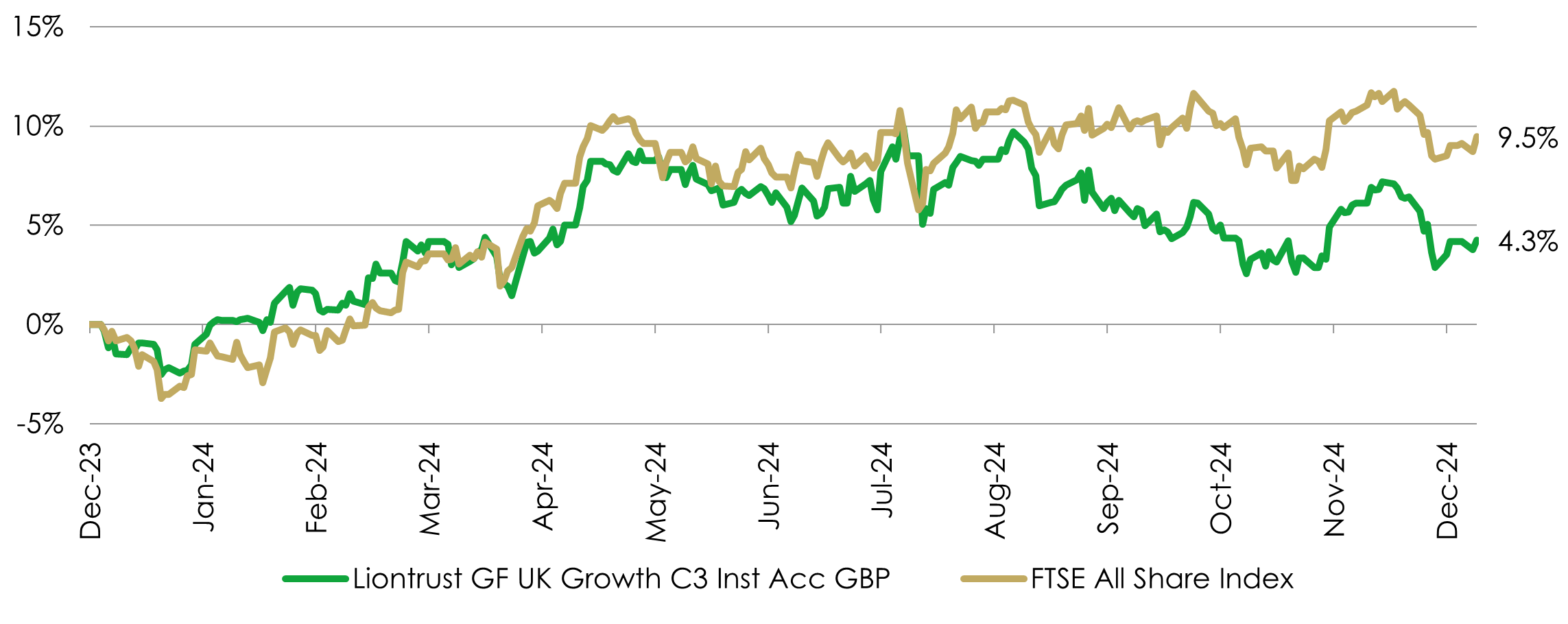

The Liontrust GF UK Growth Fund returned 4.3%* in 2024. The Fund’s comparator benchmark, the FTSE All-Share, returned 9.5%.

It was a challenging period of performance with the Fund underperforming the FTSE All Share Index by 4.7%. The Fund was tracking the market relatively closely until the end of August/September with the divergence largely developing during September and October.

2024 – fund performance versus the index

Source FE Analytics to 31 December 2024,bid-to-bid, net of fees, income reinvested, total return. Past performance does not predict future returns

We attribute the underperformance to two main factors:

- Asset allocation - lack of exposure to large cap value (Banks in particular)

- Stock specific

Taking each in turn:

Asset Allocation

Large cap value was the strongest performing part of the UK market during 2024 (MSCI UK Large Cap Value delivered a 15.0% total return). This performance was driven predominantly by two sectors – Banks and Tobacco, which collectively represent ~14% of the FTSE All Share.

The macro backdrop in terms of broader economic uncertainty and rising bond yields, in part due to concerns that inflation will remain higher than expected, has been particularly supportive for these sectors. Combined they added ~5% to the headline FTSE All Share Index return, or approximately 50% of the 9.5% gain posted during the year.

The Fund has zero exposure to Banks and therefore the cost to relative performance was the full ~4% from this sector. The Fund’s sector underweight in Tobacco (2.2% vs 3.0% on average across the year) also provided a headwind to relative performance, albeit relatively muted at 35bps.

Stock specific

There were four notable detractors during the year (each with a performance cost >60bps), each downgrading expectations and the performance impact compounded by de-rating. Two were very cyclical in nature: Spirax (-65bps) and Spectris (-65bps). Two were a combination of cyclical and company specific issues: YouGov (-82bps) and Next 15 (-72bps). The average de-rating across these five companies was particularly harsh at 35%. We retain all four of these positions and consider the recovery potential to be significant when the cyclical headwinds subside. In addition to the above the exceptional performance of Rolls Royce (total return over +90% for the year), which the portfolio does not own, had a negative attribution effect of ~1%.

Looking beyond the four detractors noted above, the portfolio as a whole performed relatively resiliently during the year with the majority of holdings delivering earnings either ahead or in line with expectations. There were notable strong positive attribution effects from portfolio holdings such as Hargreaves Lansdown, TP ICAP, Moonpig, Keywords Studios, Pearson, Gamma Communications and TI Fluids during the year, which collectively added 4.7% to relative performance.

Outlook

We are cautiously optimistic about the outlook despite a relatively uncertain macro-economic backdrop. The portfolio is, at the aggregate level, delivering healthy levels of growth, an attractive dividend yield and supported by quality fundamentals.

As at the end of December, based on market consensus, the portfolio is expected to deliver ~7% earnings growth for the year ahead. Whilst this is modestly below the long run average for the fund, in the context of an uncertain macro backdrop, we feel it is attractive and represents further recovery potential as cyclical headwinds subside. The Fund’s quality metrics are in line with long run averages across most measures.

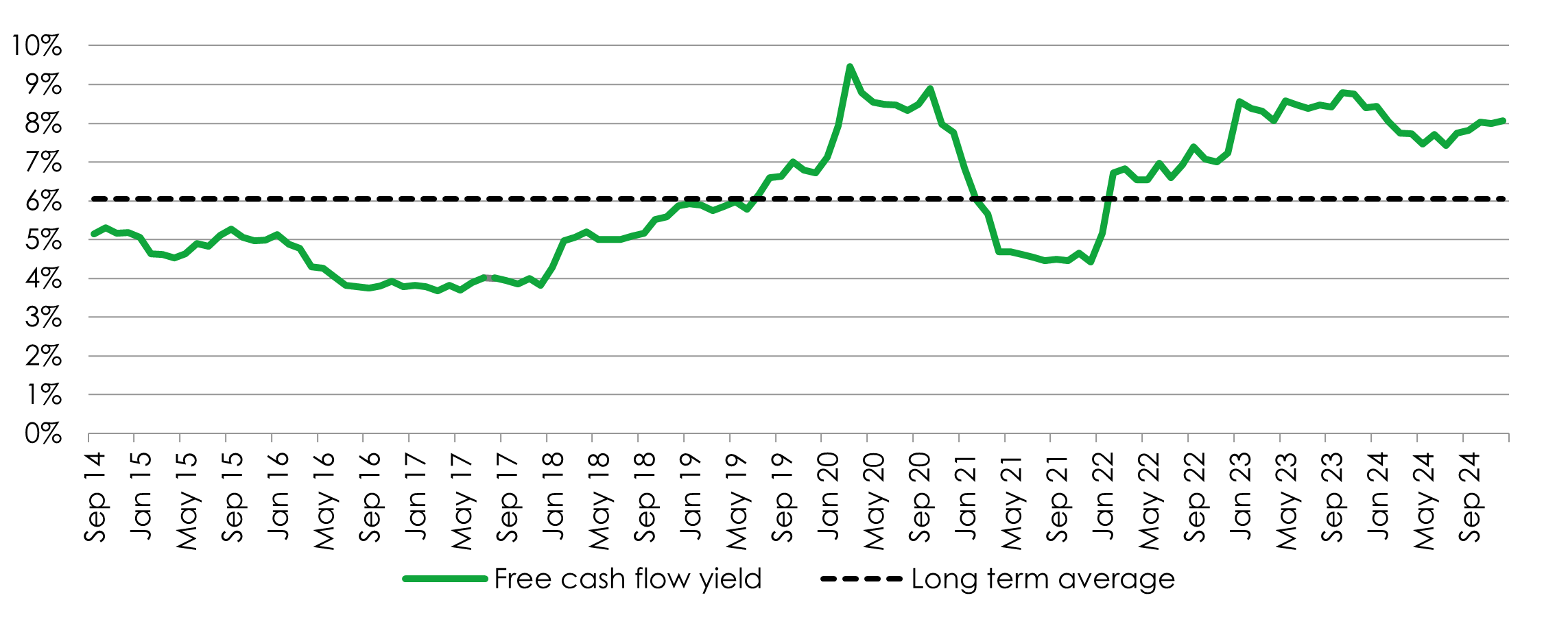

Valuations are attractive with the aggregate forward price/earnings ratio of 12x representing a discount of 14% to the long run average P/E of 14x for the Fund. A free cash flow yield of 8% is particularly compelling relative to the historic range of this metric (~1.4 standard deviations above the long run average free cash flow yield of 6.1%).

Portfolio free cash flow yield

Source: Style Analytics, monthly data points to 31 December 2024. Past performance does not predict future returns

In addition to earnings growth of 7%, investment returns for the year ahead are also set to be bolstered by a healthy dividend yield of 3%.

Portfolio valuations versus 10-year averages

Source: Style Analytics, monthly data points to 31 December 2024. Past performance does not predict future returns

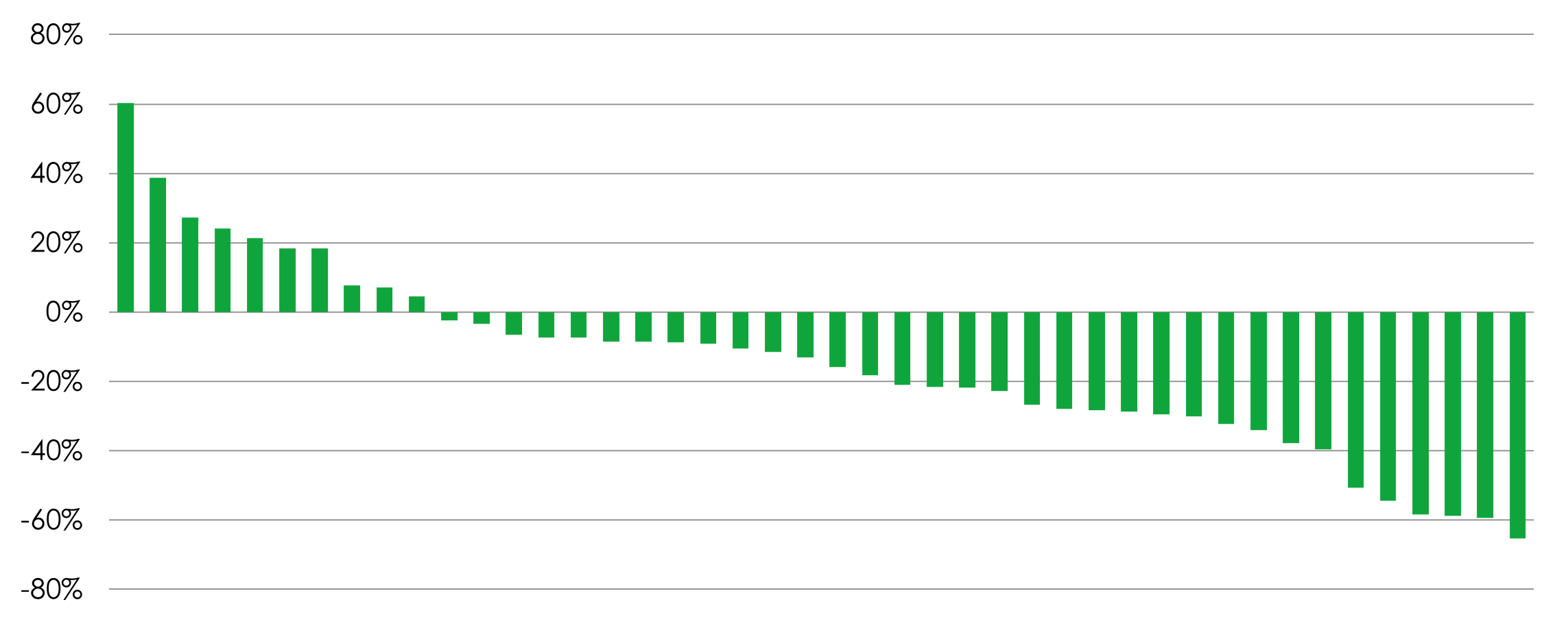

Looking at valuations at the stock level, nearly 80% of the portfolio is trading at a discount to long run averages. The average stock is on a 17% discount – this represents significant reversion potential if sentiment towards UK equities supports a re-rating back to long run averages, which we are increasingly hopefully that policy changes will help to catalyse.

Portfolio forward price/earnings ratio versus 10-year averages

Source: Bloomberg, 13.01.25. Data excludes loss making companies and companies where 12m forward EPS forecast data is unavailable. Long term average = 10 year average for each of the underlying stocks in the fund. % premium/discount is calculated by dividing the current blended 12m forward P/E ratio by the 10 year average for each stock. Past performance does not predict future returns

Discrete years' performance** (%) to previous quarter-end:

Past performance does not predict future returns

|

|

Dec-24 |

Dec-23 |

Dec-22 |

Dec-21 |

Dec-20 |

|

Liontrust GF UK Growth C3 Inst Acc GBP |

4.3% |

4.5% |

-0.4% |

21.5% |

-8.1% |

|

FTSE All Share |

9.5% |

7.9% |

0.3% |

18.3% |

-9.8% |

|

|

Dec-19 |

Dec-18 |

Dec-17 |

Dec-16 |

Dec-15 |

|

Liontrust GF UK Growth C3 Inst Acc GBP |

19.5% |

-6.4% |

13.2% |

17.0% |

9.0% |

|

FTSE All Share |

19.2% |

-9.5% |

13.1% |

16.8% |

1.0% |

*Source: Financial Express, as at 31.12.24, total return (net of fees and income reinvested), sterling terms, C3 institutional class. Non fund-related return data sourced from Bloomberg. **Source: Financial Express, as at 31.12.24, total return (net of fees and income reinvested), primary class. Investment decisions should not be based on short-term performance.

Key Features of the Liontrust GF UK Growth Fund

KEY RISKS

Past performance does not predict future returns. You may get back less than you originally invested.

We recommend this fund is held long term (minimum period of 5 years). We recommend that you hold this fund as part of a diversified portfolio of investments.

- The Fund may encounter liquidity constraints from time to time. The spread between the price you buy and sell shares will reflect the less liquid nature of the underlying holdings.

- The Fund may invest in companies listed on the Alternative Investment Market (AIM) which is primarily for emerging or smaller companies. The rules are less demanding than those of the official List of the London Stock Exchange and therefore companies listed on AIM may carry a greater risk than a company with a full listing.

- Outside of normal conditions, the Fund may hold higher levels of cash which may be deposited with several credit counterparties (e.g. international banks). A credit risk arises should one or more of these counterparties be unable to return the deposited cash.

- Counterparty Risk: any derivative contract, including FX hedging, may be at risk if the counterparty fails.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

DISCLAIMER

This material is issued by Liontrust Investment Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518552) to undertake regulated investment business.

It should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets.

This information and analysis is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content, no representation or warranty is given, whether express or implied, by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified.

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID) and/or PRIIP/KID, which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.co.uk or direct from Liontrust. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.