Perfluoroalkyl and polyfluoroalkyl substances (PFAS) are problematic and need clearing up. The Liontrust Sustainable Investment team seeks to invest in those companies helping to detect, control and destroy PFAS.

PFAS are everywhere. Also known as ‘Forever Chemicals’, PFAS are a family of over 10,000 highly persistent chemicals that resist natural breakdown. Due to their widespread use and persistence in the environment, PFAS have been found at low levels in our water, soil and bodies. Biodegradability timescales range from dozens to even thousands of years. The unique strength of the chemical structure centres around carbon-fluorine (C-F) bonds, one of the strongest and most stable in organic chemistry, making PFAS both hydrophobic (water repelling) and lipophobic (oil repelling).

But this durability comes at a cost. The cost of cleaning up PFAS is estimated to reach more than £1.6 trillion across Europe over a 20-year period[1]. Once released, PFAS compounds can be highly mobile, travelling hundreds of miles from the point of use or release. Notably, PFAS compounds bioaccumulate along food chains, binding to proteins in the blood, liver and kidneys, potentially leading to serious health concerns.

The diagram below describes the links between PFAS and several diseases and other health conditions, with examples including thyroid disease, reduced response to vaccines, kidney damage, liver damage, decreased sperm count and testicular cancer risk, to name a few.

Source: Professor Katrina Charles, Royal Society of Chemistry

PFAS enter the environment through various pathways

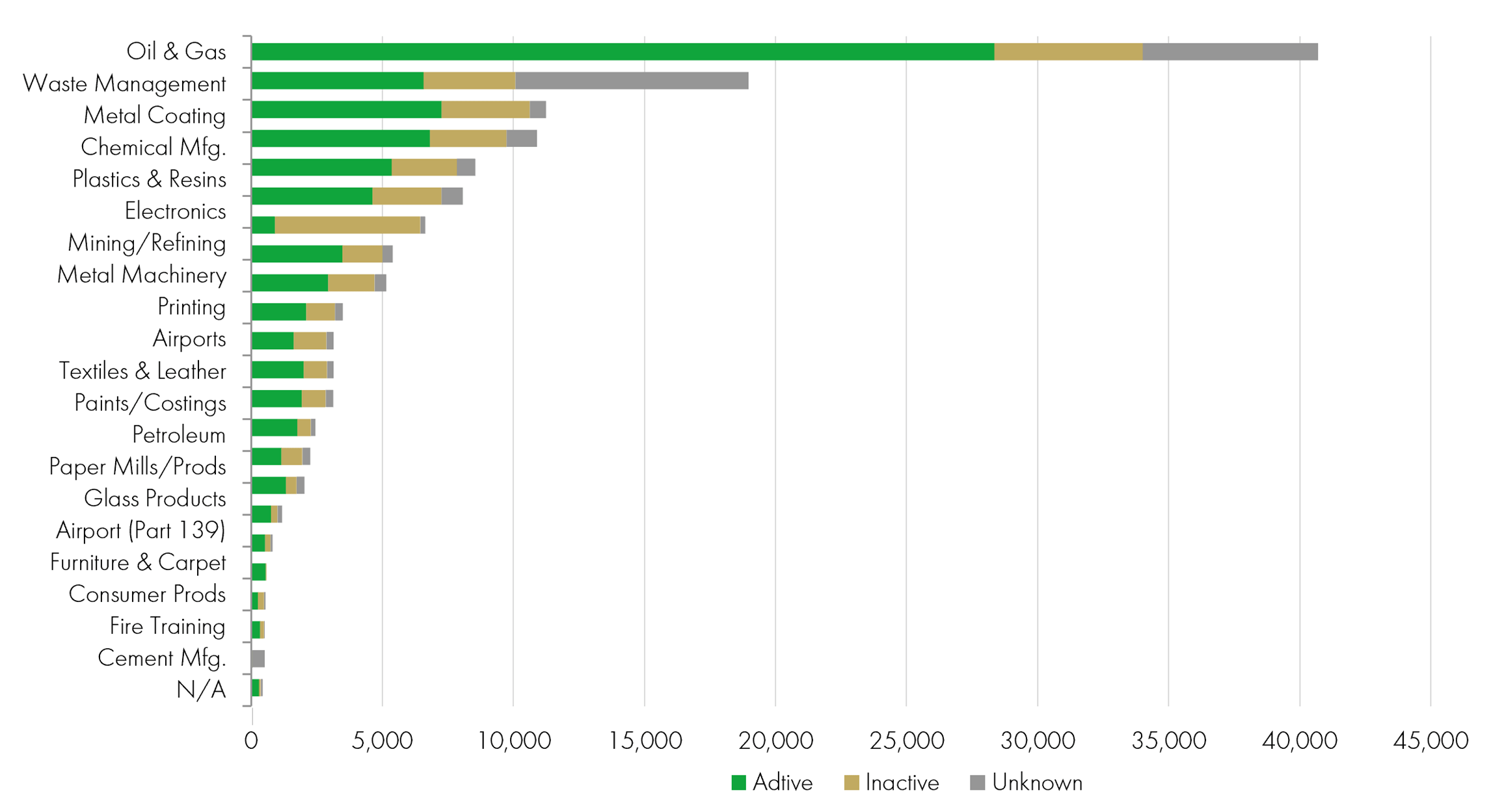

Manufacturing facilities that produce or use PFAS in manufacturing release them via emissions or effluents, the latter of which can end up in water bodies. Additionally, many everyday consumer products contain PFAS. Whether in certain non-stick cookware, waterproof fabrics, or personal care products, PFAS are found in more everyday items than most realise. Below we can see the largest industry exposure to ‘handling PFAS’, with the largest undoubtedly being oil & gas, where PFAS are used to reduce friction in hydraulic fracturing (fracking).

PFAS Report – Facilities that ‘May Be Handling’ PFAS by industry

Source: Environmental Protection Agency, Enforcement and Compliance History Online. 1) This list includes facilities that “potentially” handle, use and/or release PFAS based on their respective industrial profile. EPA has not confirmed whether each individual facility on the list actually handles, uses, and/or releases PFAS. 2) Facilities can be counted in more than one industry. 3) Data as of 1/8/2023.

Regulation is stepping up, most notably in the US

In the US, the Environmental Protection Agency (EPA) set new PFAS regulations in April 2024, limiting to four PFOA or PFOS compounds per trillion in drinking water under the National Drinking Water Standard, the most ambitious globally. To put this into perspective, the limit has come down from 70 parts per trillion between 2016-2022. Meanwhile, Europe is under discussions to introduce a blanket wide ban on PFAS in 2026, with the legislation first proposed by Germany, Denmark, the Netherlands, and Sweden in February 2023. However, draft restrictions have been met with intense lobbying efforts aimed at preventing the ban. The UK lags the US and EU on regulations targeting PFAS with Department for Environment Food and Rural Affairs (DEFRA) statements confirming that it is “currently considering the best approach to chemicals regulation for the UK”. The key legislation to date involves the limit of 100 nanograms per litre for 48 different PFAS compounds found in drinking water which came into force from January 2025. Despite mixed political willingness for regulatory adoption by geography, several industries globally are derisking their supply chain from the potential for lawsuits and large payouts by adopting solutions to test for or remove PFAS. Companies across a range of industries, from testing, to waste and consultancies are actively developing solutions to meet this demand.

In the Sustainable Investment team, we have been identifying different ways to play this theme

Publicly listed solution providers with over 5% revenue exposure to solutions around PFAS are almost non-existent. This is such a new area; with that in mind, it is highly unlikely that at this stage we’d buy a name solely dependent on PFAS exposure for long term performance success. We see being a strong solution provider as a bonus; in other words a brilliant growth arm, albeit a small one for most companies as it stands. That said, we are seeing an increasing size and frequency of M&A activity in the PFAS solution provider space, so we have set out the landscape to frame potential technologies in the M&A landscape to help us take a view on these deals, assess future revenue exposure and regulatory tailwinds.

The key investment areas include:

- Remediation (removal)

- Detection (testing)

- Consultancy

- PFAS Alternatives

- Destruction

Remediation is all about removing PFAS from the immediate environment and isolating contaminated materials (using liners or caps at landfill sites). The PFAS still exist but in a concentrated, more contained form, requiring further handling or disposal. By contrast, PFAS destruction permanently breaks down PFAS molecules into non-toxic byproducts, eliminating the compounds entirely and in doing so the environmental and health risks.

Detection involves testing water, soil, water, air or products for amounts of these ‘forever chemicals’ using sensitive lab techniques. Methods such as mass spectrometry and liquid chromatography which separate and identify PFAS molecules are used. Some tests can detect down to parts per trillion, the equivalent of detecting a drop of liquid in an Olympic sized swimming pool. Existing Sustainable Investment holdings Agilent and ThermoFisher have small exposures to PFAS testing and are both in the mass spectrometry space. Mass spectrometry is known for detecting very low concentrations of substances, making it highly sensitive. It can be applied to a wide variety of sample types, including liquids, solids and gases.

To date, ROE [2](returns on equity) have been highest in the detection space, with testing names selling analytical instruments and software benefiting from lower capital intensity.

Consultants help clients meet state and government level regulations – such as the EPA’s PFAS drinking water limits, providing services such as site or risk assessments and provide strategic and legal advisory.

PFAS Alternatives is a broad area spanning materials and chemicals designed to replace PFAS in various applications while maintaining similar performance characteristics – such as water, oil, and stain resistance – without the environmental persistence and health concerns.

Destruction is the most complex process of each of the technologies and requires highly specialised technology. It requires high capital intensity and expensive infrastructure, thus early-stage companies frequently have negative or very low ROE, with a large range between firms. PFAS destruction often rely on lumpy contracts (for example from municipalities or industrial sites), contributing to the highly fluctuating profitability. That said, given the highly specialised nature of the technology and the fact it’s the purest way to solve the PFAS problem, we assume some of the highest multiples being paid for destruction names in M&A activity.

As regulatory pressure and public awareness grows, the great PFAS reckoning is reshaping industries, creating opportunities for us in the solution providers. In this evolving landscape, identifying the winners in the clean-up economy will be key to navigating the transition from contamination to innovation.

[1] The Forever Pollution Project - Tracking PFAS across Europe

[2] ROE is net income/ shareholders equity, with shareholders equity = total assets – total liabilities

https://www.liontrust.co.uk/benefits-of-investing/guide-financial-words-terms

KEY RISKS

Past performance does not predict future returns. You may get back less than you originally invested.

We recommend this fund is held long term (minimum period of 5 years). We recommend that you hold this fund as part of a diversified portfolio of investments.

The Funds managed by the Sustainable Investment team:

- Are expected to conform to our social and environmental criteria.

- May hold overseas investments that may carry a higher currency risk. They are valued by reference to their local currency which may move up or down when compared to the currency of a Fund.

- May invest in smaller companies and may invest a small proportion (less than 10%) of the Fund in unlisted securities. There may be liquidity constraints in these securities from time to time, i.e. in certain circumstances, the fund may not be able to sell a position for full value or at all in the short term. This may affect performance and could cause the fund to defer or suspend redemptions of its shares. May invest in companies listed on the Alternative Investment Market (AIM) which is primarily for emerging or smaller companies. The rules are less demanding than those of the official List of the London Stock Exchange and therefore companies listed on AIM may carry a greater risk than a company with a full listing.

- May encounter liquidity constraints from time to time. The spread between the price you buy and sell shares will reflect the less liquid nature of the underlying holdings.

- May invest in companies predominantly in a single country which maybe subject to greater political, social and economic risks which could result in greater volatility than investments in more broadly diversified funds.

- Outside of normal conditions, may hold higher levels of cash which may be deposited with several credit counterparties (e.g. international banks). A credit risk arises should one or more of these counterparties be unable to return the deposited cash.

The risks detailed above are reflective of the full range of Funds managed by the Sustainable Investment team and not all of the risks listed are applicable to each individual Fund. For the risks associated with an individual Fund, please refer to its Key Investor Information Document (KIID)/PRIIP KID.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

DISCLAIMER

This material is issued by Liontrust Investment Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518552) to undertake regulated investment business.

It should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets.

This information and analysis is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content, no representation or warranty is given, whether express or implied, by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified.

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID) and/or PRIIP/KID, which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.com or direct from Liontrust. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.